Protecting Your Wealth

Part Two: Trusts, College and Taxation

Part One, Climbing The Wealth Ladder started this series.

Part Two is for those of you fortunate enough to find yourselves on Level 4+. Consider it supplemental information to Nick’s discussion of pitfalls.

Nick mentions the use of umbrella insurance policies to protect family assets from risks due to lawsuits and/or claims exceeding the limits of primary policies. Years ago I had one of those policies.

At the time, I owned a business that hosted training camps on open roads. Our customers included high net worth individuals, with young families.

My worst case scenario was the death of a young surgeon, with spouse and a young family. The umbrella policy was in place both for my family’s protection, and the protection of the dependents of our customers.

As well, I sat on the board of numerous companies. Often, these businesses were highly leveraged and I had personal financial exposure via my investments in the group.

My worst case scenario was: (a) losing my livelihood, (b) my connected investments going to zero, and (c) the corporate veil being pierced.

The umbrella policy bought me peace of mind, but it wasn’t cheap due to the complex nature of my life. ~20 years ago, my premiums were $5,000 per annum and the joint life expectancy of my marriage was 50+ years. Doing a bit of annuity math, my peace of mind had a future value in excess of $5 million.1

The annuity math gave me a financial incentive (and budget) to sit down with a local estates and trusts attorney and discuss options. I’m going to explain what I did but it is essential that you get tax & legal advice specific to your local jurisdiction and family’s tax position.

Trust #1 - Family Trust

I set up a fully discretionary irrevocable trust and gifted a large portion of my balance sheet to the trust. The beneficiaries of the trust are my spouse and kids.2 3 Nobody has any distribution rights and it’s not possible for any member of the family to distribute to themselves, or anyone else. There’s a lot of nuance with how you establish your trust, speak to an expert.

How much to put in the trust? I recommend you read my series on Core Capital. My choice was to put my Core Capital into the trust. Your choice is your choice. Speak to your advisors, elders and smartest friends.

Sitting here decades down the road from the settlement date, the trust is completely outside my balance sheet. Over the years, I’ve paid my own way and covered the family’s taxes/expenses. As a result, my personal balance sheet has shrunk to a couple used cars, a checking account and lot of really nice sports equipment. While someone could make a claim against me, they’re unlikely to pursue it because I don’t have material assets.

Because I administer the structure, the annual cost is cheaper than $5,000 per annum indexed to insurance-sector inflation.

Trust #2 - Unearned Capital Trust

Nick’s parents and grandparents sound like they have been exceptionally prudent with their personal finances. I expect Nick will inherit unearned capital at a future date.

Nick could consider setting up another trust. Again, there is nuance around how this trust is set up and Nick should speak with his local advisory team.

The purpose of this trust is to put a vehicle (other than Nick’s balance sheet) between himself and any potential inheritance. His spouse could set up a similar vehicle for herself. Speak to the experts about the pros & cons of including different individuals (such as all descendants of a grandparent) in the beneficiary class.

Elder wills could include language such that Nick/Spouse shall receive certain assets, unless they disclaim. In the event they disclaim then the assets shall go to the trust.

There are a bunch of reasons why your future self might want to disclaim assets into a trust that benefits yourself and your descendants. Have your advisory team explain them to you.

There are different ways to structure what I’ve just outlined. Speak with experts.

Trust #3

For Nick’s kids, when they are adults. The goal here is offer adult children the same protection you’ve given yourself. Put a trust between your balance sheet and their balance sheet.

Depending on the age gaps between generations, Nick and his spouse might desire a third trust to handle capital flows to their children at a future date.

Or… they piggyback on the Unearned Capital Trust the elders set up.

Once again… speak to the experts, they are likely to recommend you do not tie adult siblings together. Meaning the entire structure should be built so the adult families (of each generation) decide how they want to live, and raise their own kids.

Decide your values before you decide the legal structure.

Family Values Statement

Our family values statement:

All beneficiaries should be providers for themselves and their dependents as best they can in the lives they choose to lead.

The trusts are a gift to the beneficiaries to provide towards making improvements and reasonable enhancements to their lives.

Those with the responsibility for making decisions regarding distributions should be sensitive to intent without in any way restricting their full discretion.

It is hoped the family will cherish the gift and use it wisely to enhance current lives and, perhaps, the lives of future family members in a like manner.

Resource: For more reading see Wealth in Families by Collier.

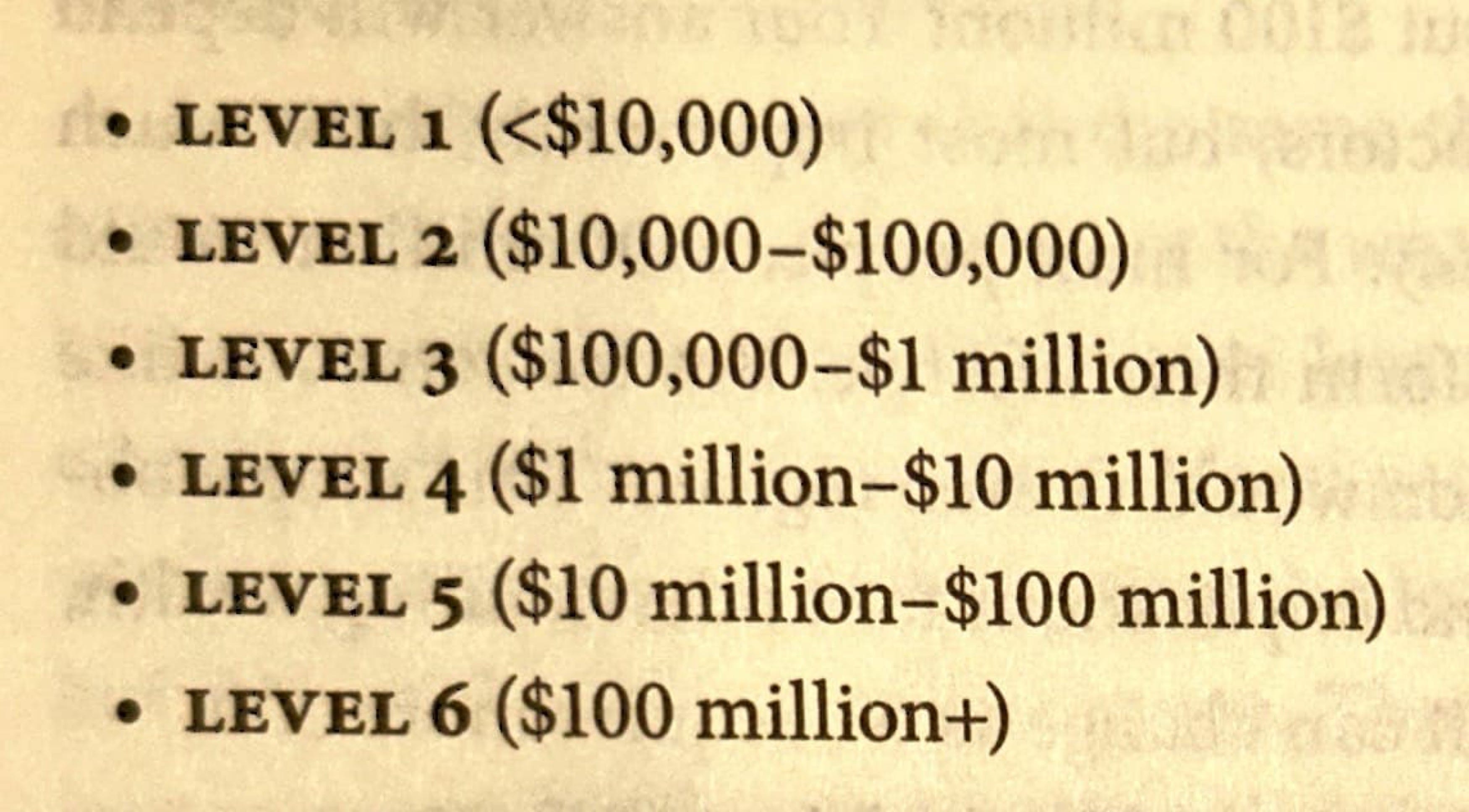

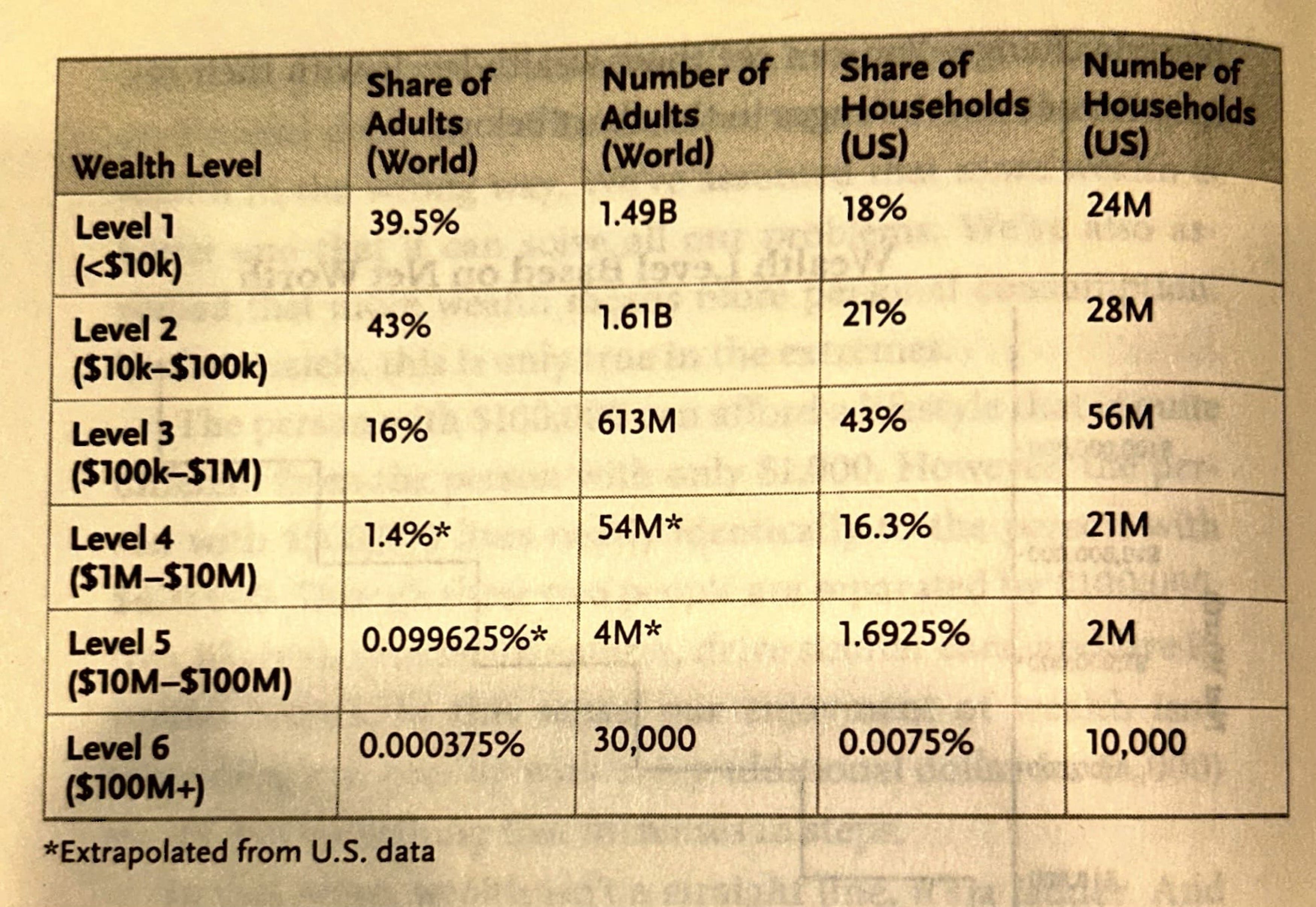

I refer to these figures in the next section. They come from Nick’s book and are repeated from Part One for your convenience.

The Price of Education

Something not discussed in Nick’s book, but huge for Level 4 families, is the cost of education. I wrote about this in Part One of My Kids & Money series.

Allow me to set the scene.

Nick’s data indicates there are ~4 million Level 5/6 individuals in the world. The exact number doesn’t matter. What does matter… your family is up against a million parents/grandparents who can pay anything for their kids/grandkids to get into any school.

On top of that, we have a longstanding US Government policy of subsidizing demand via easy debt given to students with zero thought about return on investment (for the students, the government, society or the taxpayer).

Education is like other areas where we combine regulation and subsidize demand. Well meaning policies with effects different than intended. We could fix this if we wanted.

A Level 4 family can flip the script and play a different game than the Level 5/6 families.

My deliverables to my kids:

Grow up in an area with a solid public school system.

Public through high school saves $$$ for Level 3/4 families.

These savings go into the college account, not to subsidize family consumption. Do this as early as possible.

Spend time with the family, instead of earning excess capital for them to consume.

You’ve probably gathered that I have my act together. By spending a decade sharing experiences with my kids, they’ve figured out the same thing.

Despite zero formal training, my wife has become fluent with everything you read on this site. This was due to spending time with her, having fun and doing the family financial review template.

Debt-free education to the best of their ability.

The True Cost of Debt is Hidden, please read the article with your spouse and teach it to your kids.

An incentive to neither borrow nor spend family capital for their education.

I will buy unspent college capital from my kids.4 I treat their college accounts as their money. Spending it (or not) will be my kids’ first major investment decision.

Whatever my kids don’t spend, I will purchase for the next generation. My unborn grandkids will benefit from 40+ years of tax-free compounding. I play a long game.

No guarantees of unearned capital to adult family members.

There has been a multi-million dollar cost to the family of the time I spent with them.5 That’s OK. Our family values say everyone pays their own way to live the way they want to live.

Resource: The full series on Kids & Money goes deeper.

Big Picture: Discuss this before your first kid (or grandkid) arrives.6

My Choice: When my kids were babies and preschoolers (2008-2012), I invested heavily in their 529 College Accounts. Then, I did nothing and compounding did the rest.

How Much Are You Exposed To Tax Policy?

Nick writes about the higher wealth levels being the most sensitive to taxation. I’m not so sure about that. Here’s a calculation I want you to do.

I want you to estimate all the taxes you pay.

Divide that number by your net worth.

You will get a figure expressing annual taxes paid as a percentage of net worth.

The game is making the percentage as small as possible. The smaller the number, the less impact tax policy has on your life.

++

Poor monetary policy results in inflation, which is a form of taxation on the entire population. Inflation is most painful for the lower levels of the Wealth Ladder, who don’t own assets.

If you owned assets across the Biden administration then you saw a balance sheet bump ahead of the price-of-everything going up.

We didn’t mind the initial capital appreciation bump, we were happy asset values were rising rapidly due to extremely loose monetary policy.

Then the price inflation came.

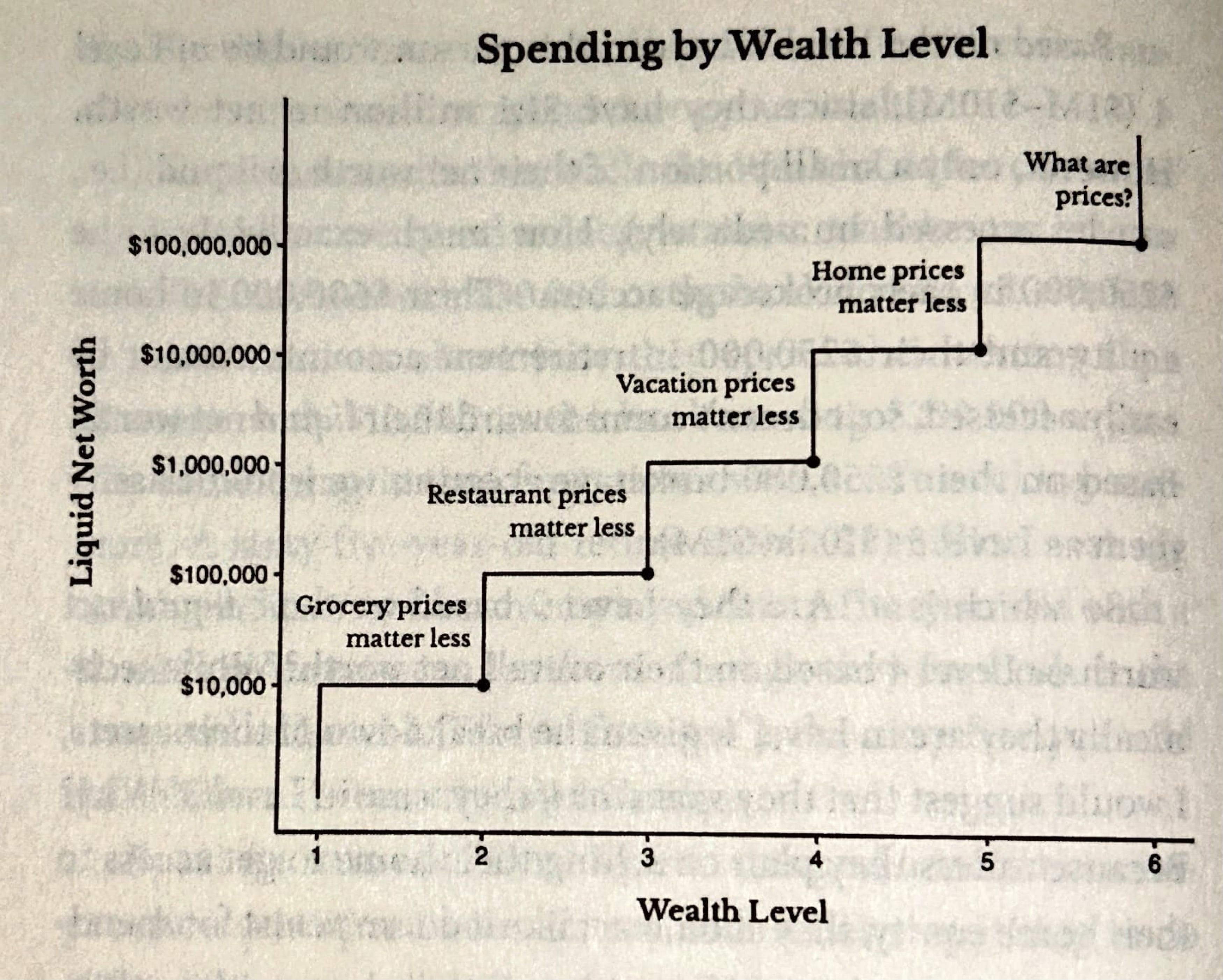

Grocery inflation is not an issue when the price of groceries is under your give-a-hoot threshold. It’s also not an issue when all you need to do is eliminate one vacation from the family budget. At the upper levels of the ladder, inflation is an inconvenience. For people at the lower levels of the ladder, it is extremely painful.

Many intelligent people are unable to follow what I explained => responsible monetary & fiscal policy most benefits:

The bottom of the Wealth Ladder, and

The most productive people working their way up the ladder.

Resource: More in my article Better Thinking About Taxes.

$5,000 payment for 50 years at an assumed cost of capital of 10%.

The trust’s definition of spouse and kids is general, there are no named beneficiaries. I prefer trusts that are fully discretionary, with no fixed distribution rights. Additionally, learn about, define and choose the Trust Protector role with care.

Everything in this article can be overseen by a corporate trustee. If you go that route then choose the President & Directors of the corporation with care. My day job is acting as the President & Fiduciary of a Private Trust Company.

If you are in the US then there is an Estate Tax angle you should have explained to you. In the meeting, have the experts explain an intentionally defective grantor trust.

As a young man, when I divorced, I re-purchased everything I wanted to keep from the matrimonial residence. As I’d previously bought the contents, most people would find this offensive. I focused solely on my desired outcome.

It’s the same thing with family capital. Yes, the capital in the college funds is there because of me. But my desired outcome is to conserve family capital and have the kids learn about return on (educational) investment.

The family paid more than a monetary cost. My nervous system is shot (but improving rapidly) from all the time I spend with preschoolers and toddlers. It was the right thing to do. No regrets.

Level 4+ families have the ability to provide social safety nets within their family systems. For example, the amount I pay in healthcare costs (for five of the healthiest people in America) is more than $2,000 per month, and set for a big rise in 2026.

Healthcare is an example of the impact of high regulation, low competition and subsidized demand. The system created by the Obama Administration has cost healthy, self-employed families billions in lost capital appreciation. Undoubtedly, there are winners on the other side of the ledger. Just like inflation, most people are oblivious to the wealth transfer out of their family due to our decisions on healthcare policy.