Climbing The Wealth Ladder

Insights from Nick Maggiulli's New Book

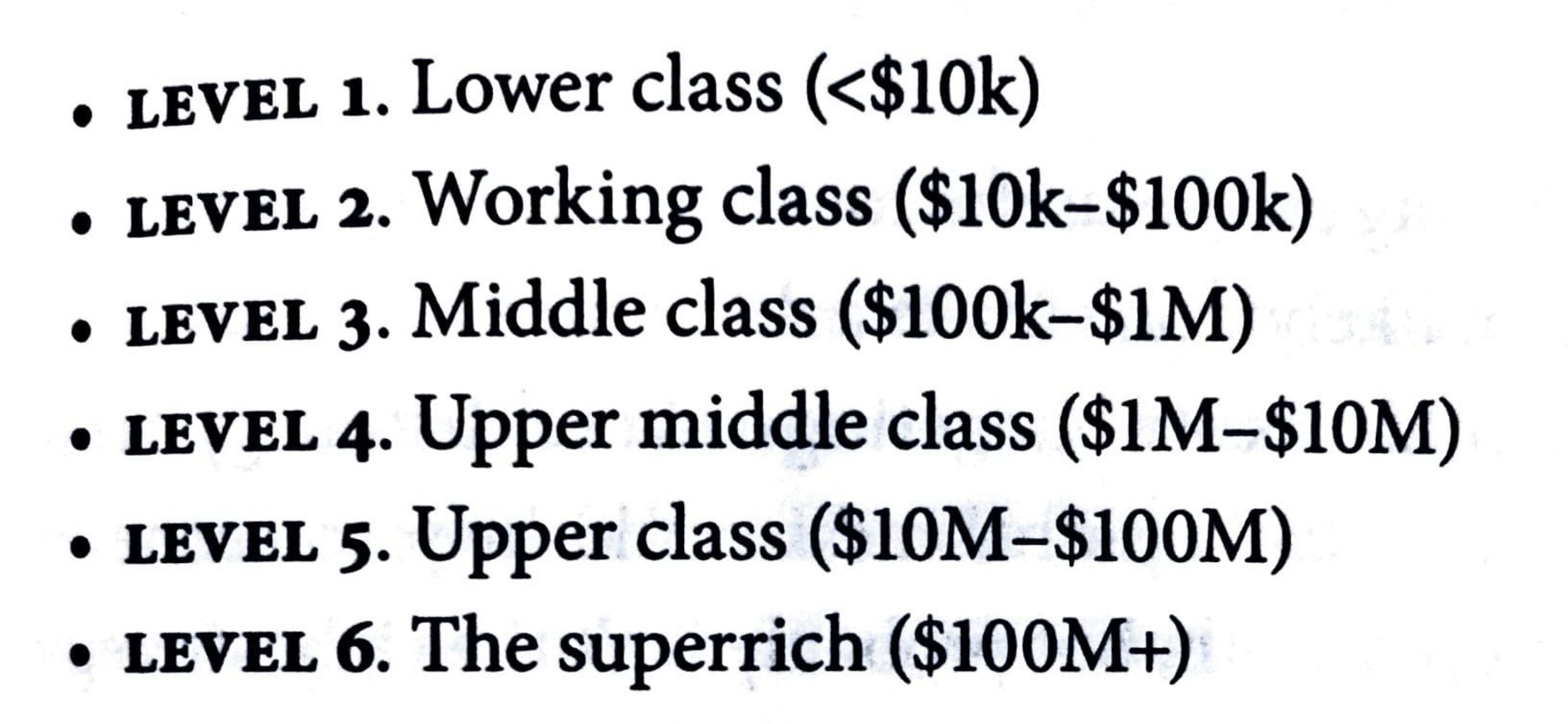

Nick Maggiulli’s new book, The Wealth Ladder, frames wealth via six distinct levels. As we climb, the challenges and strategies evolve, requiring new approaches to achieve financial success. I’m going to highlight key concepts from Nick’s work, link you to supplemental resources, and share personal insights to help you navigate your wealth journey.

Wealth in Time

Nick defines wealth levels by net worth. Once you’ve calculated your net worth, bring time into the frame. A practical way to do this is by calculating Wealth in Time:

Net Worth ÷ Core Cost of Living = Wealth in Time

For example, a middle-class family with a $500,000 net worth and a $75,000 annual cost of living has a Wealth in Time of 6.7 years. This metric connects net worth, spending, and time. Wealth in Time is a useful concept when considering different strategies and courses of action.

Resource: Explore my article on The Money Value of Time for a step-by-step guide.

Power Laws and Wealth Distribution

Nick’s Wealth Ladder follows a power law, where each level requires a tenfold increase in net worth. In 2025, this base-10 model fits well to illustrate wealth dynamics. Nick’s book simplifies wealth distribution into three tiers:

Bottom: 40% of the population

Middle: 40%

Top: 20%

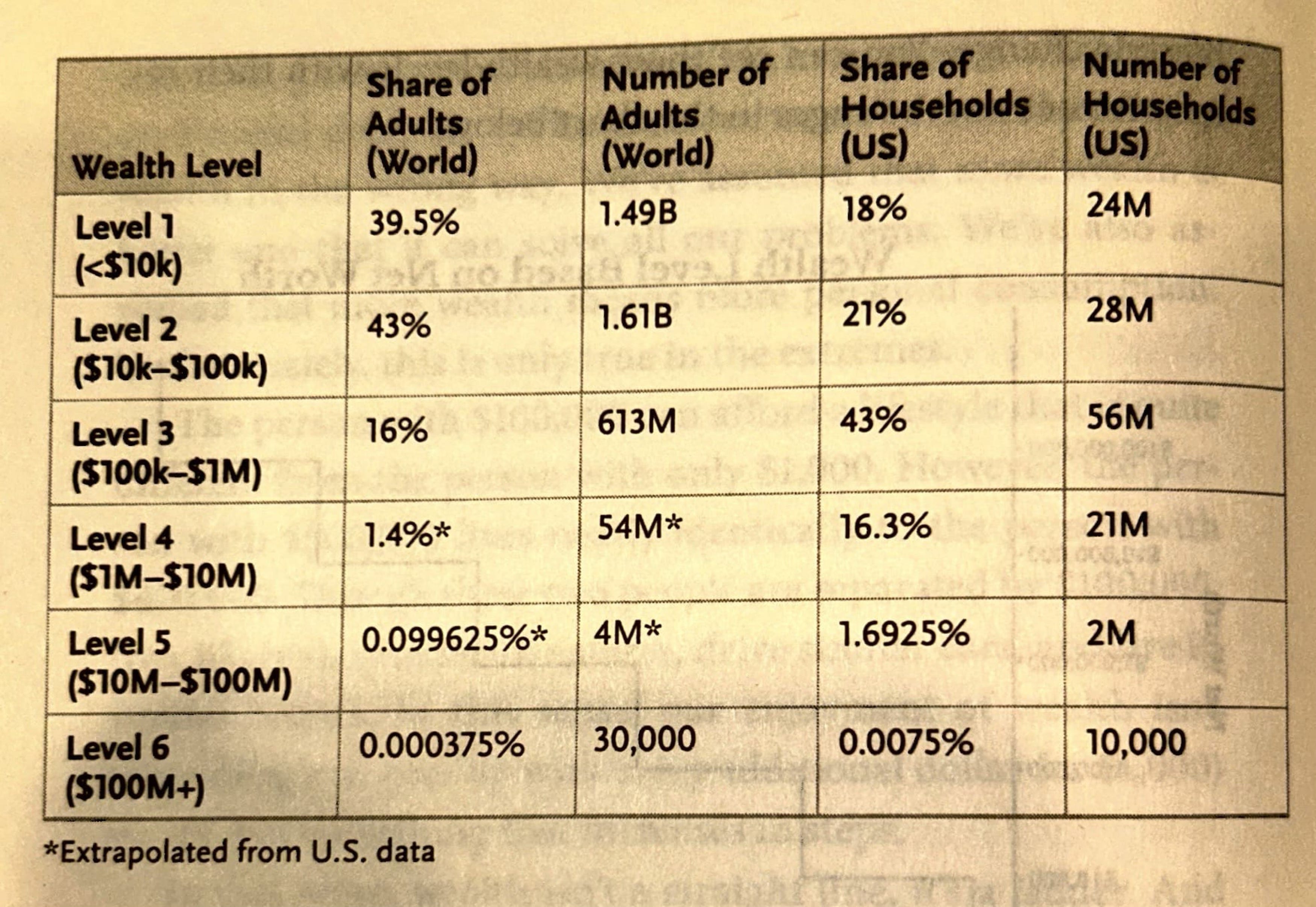

Wealth distribution is scale-invariant, meaning the 80:20 (Pareto) ratio persists at every level. For example:

Globally, Levels 1 and 2 represent 80% of wealth holders versus the top 20%.

In the U.S., Levels 1, 2, and 3 form the bottom 80%, with the top 20% at higher levels.

This pattern explains why most people feel “middle class” within their peer group, a quirk of human perception amplified by power laws. We tend to look up the distribution, comparing ourselves to those with more wealth, beauty, or status.

Resources:

My article, Victory & Vanity, explains our default programming.

For ideas on reprogramming our default instincts, read Virus of the Mind by Richard Brodie.

Escaping Lower-Level Thinking

When I run into someone who’s trapped in lower level thinking, I ask them,

Why did you want the money you have?

Many assume more money is always better. The book is filled with examples of when more is better, and when more is not better.

I agree with Nick’s conclusion in this section.

In Levels 1 and 2, more wealth is much better.

In Level 3, more is better.

From Level 4 onwards, more has diminishing returns.

Others seek money as a proxy for something quite different (respect, deference, status…). Those people do better aiming directly towards their core need(s).

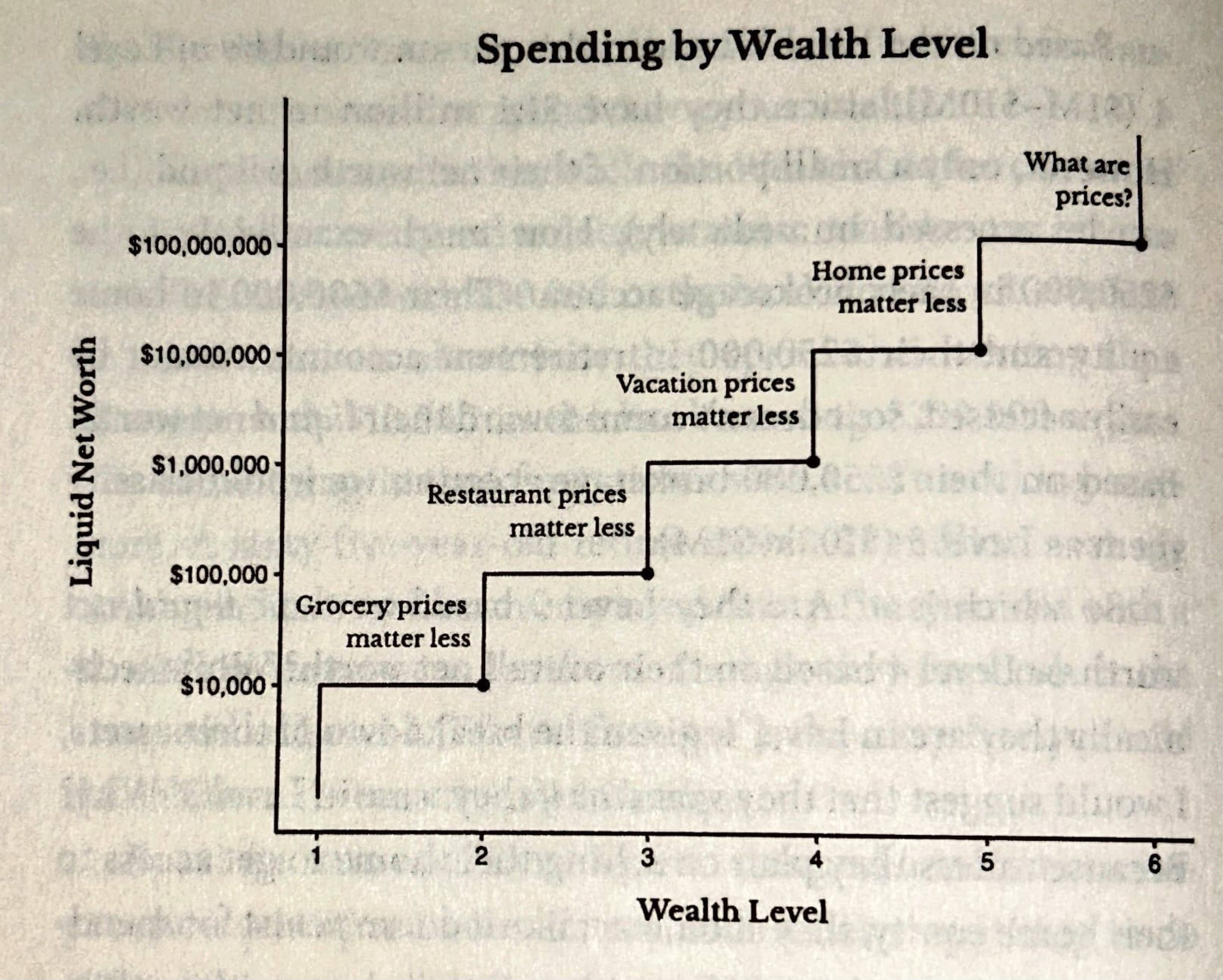

One way money makes my life significantly better is I can afford not to think about stuff. What stuff am I not thinking about? That depends on our level.

I’m sure we’ve all met someone far above Level 2 who worries about grocery prices. I used to be one of those people. It takes effort to leave lower level thinking behind. We all have quicks when it comes to spending. Here’s one of mine…

My marriage has an inside joke about a time when I freaked out about the price of Bermudian strawberries. In my defense, it was 20 years ago and there’s been a lot of inflation since 2005.

To this day, whenever I’m surprised by a price, I say to my wife…

Eight bucks for strawberries?!?

The point here. If we want to move up the ladder then we need to focus on things that move the needle. If you’re Level 3/4/5 then gasoline, grocery prices, restaurant prices… are a distraction from what matters.

Another example, something I would say to my family when we were skiing.

The decision is not whether, or not, to order the $8 fountain drink.

The decision is whether, or not, to be a ski family.

Too many people focus on the fountain drink, rather than lifestyle inflation and the environment around the next generation. The environment around our kids becomes our family’s future baseline.

Resource: Read my Environment article (Part 4 of a five-part series) for tips on intentional lifestyle design.

Nick’s 0.01% Rule

To avoid sweating the small stuff, I set a “give-a-hoot” threshold.

Nick’s version of my threshold is called the 0.01% Rule and suggests ignoring expenses below 0.01% of net worth. For a $500,000 net worth, that’s $50.

When I met my wife, my threshold was $5,000—far above Nick’s rule, given my lower net worth at the time. This policy saved time and emotional energy, though not money.

Why did it work?

I knew where to cut spending with minimal emotional cost.

Multiple income streams allowed me to cover gaps (see Nick’s Just Keep Buying for strategies).

My high Wealth in Time provided a buffer.

I saved 50% of my income, a superpower for young people.

Resource: Use my article, Knowing Exactly What You Want, to discover what you want from money.

The Price of Attention & The 1% Rule

In my late 20s, at the top of Level 3 (inflation-adjusted), I shifted my decision making criteria towards time & emotion. Educated in finance and full of energy, I realized wealth-building could crowd out other “ladders” such as marriage, knowledge, and community.

When we are focused on moving up the wealth ladder, we are not focused on the other ladders available. There are many ladders available to us:

Marriage

Knowledge

Athletics

Community

Service

Parenthood

Teaching

Our best opportunities can lie outside our current frame of reference. I’ve found it useful to keep empty space in my life so I can see, then seize, those opportunities.

One of those opportunities was a business idea I had during a dinner with a friend. The idea was converted into a new company, which eventually generated a large return on investment. I made the equivalent of 20-years spending because I had a life structure that enabled me to focus exclusively on a single new idea.

Nick’s 1% Rule advises ignoring opportunities that don’t increase net worth by 1%. My urge you to go way further:

At Level 3, seek opportunities that buy years of wealth.

At Level 4, treat time, attention, and emotion as the true cost of opportunities. You are financially secure. The game now involves avoiding ruin via substance abuse, legal trouble, infidelity, or excessive leverage.

At all levels, prioritize health, strength, and vitality as you age. Ultimately, relationships matter most.

Resources:

Read about Core Capital to understand your financial needs and protect your Core Capital.

My Greatest Hits contain insights for balancing financial wealth with a life well lived.

Next: Four things related to the Wealth Ladder.

Kids,

The Price of College,

Trusts, and

Taxation.

Great, simple rules to stay focused on what matters most and make decisions with clarity, without getting caught up in the emotions around money, whether self-imposed or influenced by others. Thanks for sharing, G.

Great article. Actually one day realizing that selling my time for (decent) money is actually preventing me from getting above your level 3 was a hard lesson…..Now I spend a lot of time making DEA tables, Delegate, Eliminate, Automate, quite tough for someone who prides himself more for personally being in the dirtiest trenches rather than back in the command post….